What happened?

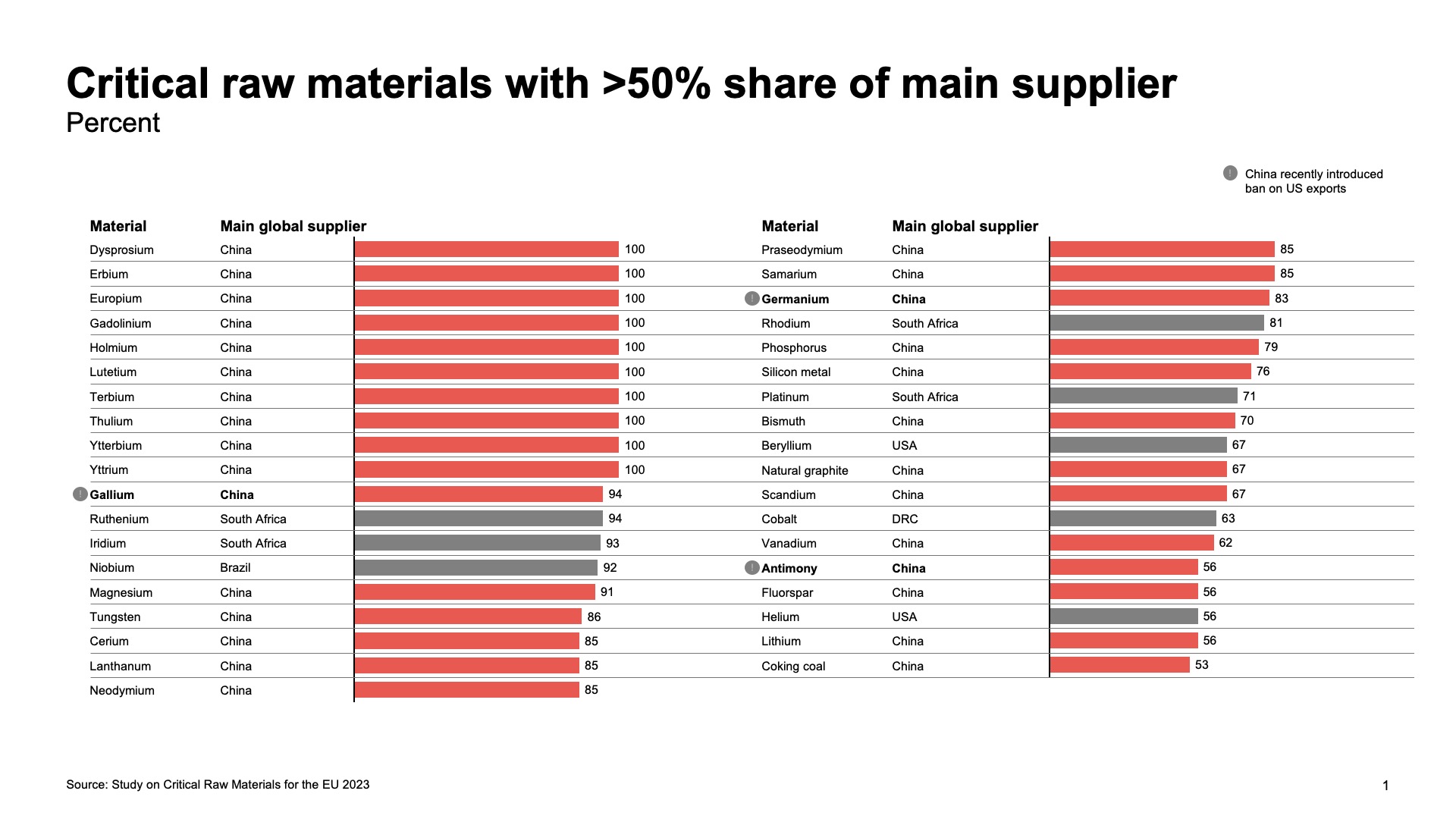

In early December 2024, China, the largest miner and refiner of critical raw materials, announced a ban on exports of three minerals – gallium, germanium, and antimony – to the United States, adding a new element to the escalating tech trade restrictions between the two countries. China currently controls 94% of the global supply of gallium, 83% of germanium, and 56% of antimony.[1] This ban builds upon existing export controls imposed already in August 2023.[2]

Why is it important?

China’s restrictions on gallium and germanium exports highlight worries about the dependability of critical mineral supplies vital for economic growth, national security, and the shift to renewable energy sources. Given the significant dependence on China for these materials and the intensifying trade and technology competition between the US and China, the prospect of additional restrictions seems highly plausible.

What are these materials used for?

Gallium, germanium, and antimony are critical minerals with diverse applications across multiple industries, including semiconductors, telecommunications, and defense.

Gallium and germanium are vital in producing advanced semiconductors. The uses include:

- radio frequency electronics (for example, radio frequency power amplifiers for mobile handsets and wireless area networks)

- power electronics (for example, direct current to direct current [DC–DC] converters, onboard chargers, and traction inverters in electric vehicles)

- photonics (lasers, lidar applications)

- light-emitting diodes (LEDs) for lighting and displays

- high-efficiency solar cells, mainly in space solar photovoltaic (PV) cells.[3]

Antimony is widely used to enhance the hardness and strength of other metals, a property particularly valuable for defense applications such as shielding materials and bullets. Other military uses include night vision goggles, explosive formulations, flares, nuclear weapons production, and infrared sensors.

Antimony has also become critical for electrical and energy related technologies, including semiconductors, batteries, and cables.[4][5]

What is the scale of dependency on China?

China is the largest global supplier of a wide range of critical raw materials.

Both gallium and germanium are heavily dependent on supply from China, although alternative sources are available in countries such as Germany, Kazakhstan, Ukraine, Russia, and Canada.[7] These minerals can also be obtained from zinc and/or aluminum concentrates through secondary extraction circuits within smelters, which already exist or could be added to existing facilities across North America and Europe.[8]

Can the supply of these materials be diversified?

Germanium

The supply of germanium could likely be diversified. For example, a mine in Alaska, one of the world’s largest zinc producers,[9] produces germanium as a byproduct and supplies to the North American market. Representatives have indicated they are considering increasing the germanium production in light of the recent ban.[10] In the Democratic Republic of the Congo, the state-owned mining company has invested in a new smelter and announced its first germanium exports to Europe.[11]

Gallium

For gallium, diversifying supply can be achieved by expanding gallium production capacity at smelting/refining facilities for gallium recovery from existing zinc concentrates which would enable a rapid ramp-up in gallium production.[12] For example, a zinc smelter in Tennessee is considering expanding its capacity to produce both gallium and germanium.[13]

These approaches are not currently pursued due to economic reasons. The overall margin improvement from gallium and germanium extraction does not offset the investment required for infrastructure installation or expansion for private players. To incentivize production additions, potential margins would need to increase, either through higher realized prices or changes in underlying costs.[14]

Antimony

For antimony, the second-largest supplier after China is Russia, accounting for 18% of the global supply. Other large suppliers include Tajikistan (approximately 15%), Australia (around 3.5%), and Myanmar (around 3.5%).[15] To diversify the supply chain, producers can accelerate antimony extraction from existing and “shovel-ready” gold, copper, and silver mines with trace of antimony content.[16] For example, in the United States, a single Idaho-based gold mine with access to antimony sources could potentially meet approximately 35% of U.S. demand, based on the project’s ambitions.[17]

Experts suggest that China’s recent export ban also reflects a clear ambition to impose more stringent end-use reviews for other critical materials, such as graphite.[18]

The GLOBSEC GeoTech Center will continue to examine the role of critical raw materials and the impact of related global dynamics on economic and national security in the U.S., Europe, and worldwide.

[1] Based on data from Study on Critical Raw Materials for the EU 2023 (https://op.europa.eu/en/publication-detail/-/publication/57318397-fdd4-11ed-a05c-01aa75ed71a1). Germanium supply in 2024 is more diversified due to Gecamines exports to Europe.

[2] See: https://www.reuters.com/markets/commodities/china-bans-exports-gallium-germanium-antimony-us-2024-12-03/

[3] https://pubs.usgs.gov/publication/ofr20241057/full?utm_source=chatgpt.com#ofr20241057-a1

[4] https://www.usitc.gov/publications/332/executive_briefings/ebot_a_critical_material_probably_never_heard_of.pdf

[5] https://www.csis.org/analysis/chinas-antimony-export-restrictions-impact-us-national-security?utm_source=chatgpt.com

[6] https://op.europa.eu/en/publication-detail/-/publication/57318397-fdd4-11ed-a05c-01aa75ed71a1

[7] There are also other known producers, e.g., Japan, Slovakia, USA, and Belgium

[8] For details, see the respective sections of the USGS Mineral Commodity Summaries: https://pubs.usgs.gov/publication/mcs2024

[9] See: https://www.miningnewsnorth.com/story/2024/10/25/news-nuggets/red-dog-is-producing-5-percent-of-worlds-zinc/8767.html

[10] See: https://www.reuters.com/markets/commodities/rattled-by-china-west-scrambles-rejig-critical-minerals-supply-chains-2024-12-06/

[11] See: https://www.reuters.com/markets/commodities/congo-state-miner-gecamines-announces-first-germanium-exports-europe-2024-10-14/

[12] See: https://cepa.org/article/china-gallium-and-germanium-the-minerals-inflaming-the-global-chip-war/

[13] See: https://www.wsj.com/business/tennessee-zinc-smelter-is-at-the-center-of-u-s-china-trade-fight-dd370fba

[14] See: https://cepa.org/article/china-gallium-and-germanium-the-minerals-inflaming-the-global-chip-war/

[15] See page 12: https://perpetuaresources.com/wp-content/uploads/Perpetua-Resources_Investor-Presentation_October-2024.pdf

[16] See: https://www.spglobal.com/commodityinsights/en/market-insights/latest-news/metals/082324-interview-china-antimony-export-restrictions-exacerbate-global-supply-fears-usac

[17] See: https://perpetuaresources.com/antimony/

[18] See: https://www.reuters.com/markets/commodities/china-bans-exports-gallium-germanium-antimony-us-2024-12-03/